Panther Creek Plats

Michael Stoner Tract

Boger Tract

by

Keith McDowell

Keith McDowell

Introduction

The following analysis by the author of land records in Rowan County NC is presented to the general public for consideration. Comments are welcomed by the author. Note that the analysis is very detailed and requires careful attention to the figures.

Presentation

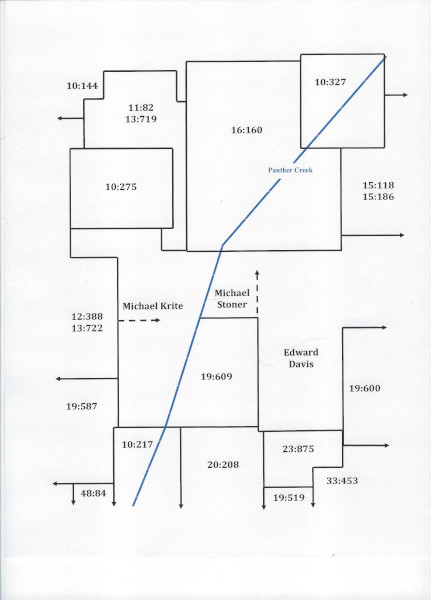

A family of plats along Panther Creek in Rowan County present a major challenge to genealogists due to an absence of deeds, court records, and estate papers. Indeed, at least two major tracts of land are nearly invisible as to record keeping. One such tract of land is the property of Michael Stoner which amounts to nearly 400 acres and is owned by him or his widow from about 1800 until the 1830s. Another is a tract of land known as the Boger Tract containing nearly 300 acres of land and owned by a Daniel Boger who died in 1826 possessed of the property. The Boger Tract remained in the Boger family until 1855 when it was finally divided among the heirs at Law or other claimants. The story of these two tracts and the surrounding family of plats, which we call the Panther Creek Plats, is the essence of this presentation.

The Rowan County deeds used to construct the framework for the Panther Creek Plats are listed in the following table.

Table: Panther Creek Early Deeds

DB10:144 10 October 1783 264 A - State Grant No. 372 to Francis Hoffman

DB10:217 10 October 1783 200 A - State to Frederick Fennell

DB10:275 4 May 1784 200 A - State Grant No. 960 to Robert Weakley

DB10:327 4 November 1784 200 A - State Grant No. 1640 to Frederick Fisher

DB11:82 25 October 1786 111 A - State Grant No. 1103 to John Basinger

DB13:719 27 November 1793 110 A - State Grant No. 2248 to John Basinger

DB15:118 7 March 1795 318 A - David Woodson to Michael Krite

DB19:519 21 December 1801 152 A - State to Hugh Horah

DB19:587 31 August 1805 233 A - Sheriff George Fisher to Daniel Clary

DB19:609 14 October 1805 207 A - John Hudson to George Davis

DB19:600 29 January 1806 341 A - David Woodson to Enoch Phillips

DB20:208 6 May 1811 200 A - John Bame to John Cauble

DB23:875 23 July 1816 90 A - Peter Lyerly to Martin Miller

DB33.453 28 November 1828 560 A - Joseph Pearson to John Morgan and Guy Hill

For the most part, the metes and bounds of these various deeds fit together in a straightforward manner with several notable exceptions as shown in Fig. 1. In the first instance, the two State Grants DB11:82 and DB13:719 to John Basinger coupled with the State Grant DB10:275 to Robert Weakley are incorrectly rendered on both the Rendleman plat map[1] and the Kurtz plat map[2] for this region of Morgan Township. Furthermore, their renderings don't match up with subsequent deeds or land records such as the 1888 division of the lands of Jesse Ribelin as discussed below. Secondly, we have used information from subsequent deeds and land records to be described below to properly orient the northern tier of plats with the southern tier noting that only one line connects the two tiers in Fig. 1.

The southern tier of plats in Fig. 1 along their northern edge presents a serious challenge to genealogists due to the absence of registered deeds, court records, and estate documents. However, that challenge can be met for the most part through a careful and detailed reading of the existing records.

To begin that analysis, we comment first on what is actually known about the real estate west of Panther Creek and displayed in Fig. 1 with the name "Michael Krite." Quoting from deed DB13:722, the State Grant to John Hess, we find the following language:

thence North at 28 Chs & 50 links to a Small Post Oak Michl Krites Corner then at five Chs his other Corner black Jack Oak in all Sixty Chs to a black Jack Oak

Other than a repetition of the same language by surveyors in several other deeds, this is the only reference to the Michael Krite plat. Both Rendleman and Kurtz draw a boundary line from this corner East to Panther Creek adjoining a plat of Michael Stoner East of Panther Creek, but there is no evidence to support such a rendering. Indeed, as shown below, Michael Stoner is reported in the 1796 tax list for Capt. Fisher's Company[3] with 200 acres of land in close agreement with the 202 acres reported by Jesse Ribelin in the 1855 tax list of Capt. Levi Trexler[4] and the 1888 division of his land.[5] That division of land clearly contains the Michael Stoner land East of Panther Creek as discussed below as well as property West of Panther Creek. We conclude that Michael Stoner owned property on both sides of Panther Creek. This revelation is essential to understanding the location of various land plats. It is certain that Michael did own a considerable amount of real estate as shown by his tax records in the following table.[6, 11]

Tax Listings of Michael Stoner

1796 - 1 WP 0 BP 200 - Capt. Fisher's Co.

1803 - 1 WP 0 BP 250 - Capt. Lyarlie's Co.

1804 - 1 WP 0 BP 350 - Capt. Creson's Co.

1807 - 350 - Capt. Creson's

1809 - 350 - Capt. Bower's Co.

1810 - 350 - Capt. Bower's Co.

1812 - [blank] - Capt. Pool's Co.

1814 - 400 [Likely value, not acerage] - Capt. Pool's Co.

1815 - 390 (300.90) - Capt. Ja. Pool's Co.

1823 Widow Stoner - 390 - Capt. M. Miller's Co.

1830 Widow Stoner - 390 - Capt. Isaac Ribelin's Co.

Another factor to consider is that Michael Krite died sometime in late 1799 or early 1800 as shown by the following court records.[Note that P&QS stands for Pleas and Quarter Sessions court miniutes available at the North Carolina State Archives.]

Ordered that Michael Krites administrators sell a negro woman named Cilia belonging to said Estate.

Rowan P&QS: Friday 9 May 1800, page 8

Rowan P&QS: Friday 9 May 1800, page 8

It is also known that Michael Krite is survived by several heirs as shown by court records.

George Crite orphan of Michael Crite decd being of lawful age came into Court and chose Frederick Fisher his guardian and gave bond with Jacob Brougher in £400.

Rowan P&QS: Wednesday 6 August 1800, page 28

Rowan P&QS: Wednesday 6 August 1800, page 28

Also, George Fisher Esqr be appointed Guardian of Kitty Krite daughter of Michael Krite decd.

Rowan P&QS: Tuesday 3 November 1801, page 134

Rowan P&QS: Tuesday 3 November 1801, page 134

While these records reveal nothing about the disposition of the real estate of Michael Krite, it is certain that he had heirs and that actions would have been undertaken during this time period with respect to said property. It is interesting to note that the tax listings for Michael Stoner report 250 acres in 1803 in Capt. Lyarlie's Company and 350 acres in 1804 in Capt. Creson's Company. It's possible that the 250 acres in the transcription of the tax records for 1803 should be 350 acres since that number is consistently report by Stoner in several tax listings. By 1815, Stoner reports 390 acres in two tracts of 300 acres and 90 acres. That acreage continues to be reported by his widow through an 1830 tax listing. We suspect that the 300-acre tract contains the 1888 Jesse Ribelin tract as well as the remainder of the Krite land West of the Ribelin tract. That acreage measures out to be very close to 300 acres. The 90-acre tract likely adjoins this tract to the South and on the West side of Panther Creek. This contention is based on the reporting by George Crotzer of a 90-acre tract. We discuss that tract below.

In the original deeds used to construct our Panther Creek plats, the real estate of Michael Stoner is described as follows from deed DB19:609 dated 20 March 1803 of John Hudson to George Davis.

Beginning at a small maple standing in the East bank of the Creek in Jacob Frick's line and running thence East forty six chs and fifty six links to a Black Oak Edward Davises corner thence with his line North fifty four chs and fifty links to a pine Michael Stoners corner thence with Stoners line West twenty nine chs and fifty links to a stake in the

aforesaid bank of the Creek thence up Panther Creek as it wanders to the place of the Beginning containing in the whole two hundred and seven acres of land

This description and it's repetition in subsequent deeds for the same property clearly indicates that Michael Stoner owns land East of Panther Creek and North of this plat. We display this in Fig. 1 by a dashed arrow pointing North, even though we know from subsequent information as presented above more about the Stoner plat.

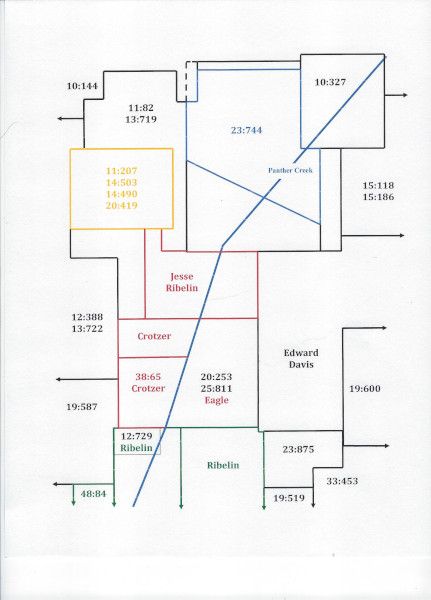

Following the purchase of the 207 acres by George Davis, he sells the land to John Mull, although a deed has not been found. We display this transfer in Fig. 2 with the name Eagle. The metes and bounds of subsequent deeds relevant to our presentation mention the Mull property even though he owns the tract for only a short period of time. It is therefore important that evidence be introduced proving that Mull obtained the property from Davis.

Circumstantial evidence demonstrating the transfer of the 207 acres from Davis to Mull can be found in the tax records. In the 1803 tax records for Capt. Lyarlie's Company,[7] George reports 207 acres. In the 1807 tax listing for Capt. Creson's Company, George again reports the 207 acres. In the 1809 tax listing for Capt. Creson's Company, John Mull reports the 207 acres and George Davis is not listed.

Further and conclusive proof that John Mull indeed obtains the 207-acre tract is found in the description of the metes and bounds of deed DB20:253 dated 8 August 1811 where he sells the 207-acre tract to John Knup Senior.

… on the East side of Banther [sic] Creek Beginning at a small maple standing on the East Bank of the creek in Jacob Fricks line and running thence East forty six chains and fifty links to a Black Oak Edward Davises corner thence with his line North fifty four chains and fifty links to a pine Michael Stoners corner thence with Stoners line West twenty nine chains and fifty links to a stake in the aforesaid bank of the Creek thence up Banthers Creek as it menders to the place of the beginning containing in the whole two hundred and seven acres of land

John Knup Senior died and left a Will dated 20 December 1815.[8] In his Will, he devised his Panther Creek property in an equal division to his two sons, John and Leonard. On 21 September 1819 in deed DB25:811, John sells his portion to his brother Leonard.

… on the waters of Panter [sic] Creek joining the lands of Jacob Frick, Henry Bever, John Kauble, John Beam containing two hundred and seven acres to which the said John Knup is entitled to the one half of by the will of his father John Knup Senr Decd

The lands of John Kauble and John Beam [sic Bame] relate to deed DB20:208 on the southern boundary of the 207-acre plat. We discuss the Frick land below. Efforts to find out whether the land of Henry Bever/Beaver is on the eastern or western border of the 207-acre have so far not met with success.

Numerous records including the 1830, 1840, and 1850 census records demonstrate that Leonard Knup moved to Union County IL during the 1820s. Unfortunately, no records have been found documenting in what manner Leonard disposed of the 207-acre tract. However, by the 1838 tax list for Capt. Levi Trexler's Company,[9] Solomon Eagle reports the 207-acre tract. He continues to report the tract through the 1840s and on the 1855 tax list for Trexler's Company[4] where the property is described as being on Panther Creek. As shown below by various metes and bounds of the adjoining properties, it is clear that the 207-acre tract becomes the property of Solomon Eagle by 1838 and remains his property into the 1850s. In Fig. 2 we label this tract of land with the name "Eagle" using red font.

We turn next to the 200-acre tract of land labeled "10:217" in Fig. 1 and owned initially by Frederick Fennell via a State Grant dated 10 October 1783.

… on both sides of Panters [sic] creek joining Moris Read Begining at a pine on the south side of the creek and runs East crossing the creek thirty three chs & fifty links to a white oak thence North sixty chs to a black Oak thence West thirty three chs & fifty links to a post oak thence south sixty chs to the Begining.

Fennell sells the property to Jacob Frick on 26 May 1792 in deed DB12:729.

On both sides of panters Creek [sic] joining Moese Road Begining at a pine on the South side of the Creek and runs East crossing the Creek thirty three Chains and fifty Linkis to a white Oak thence North sixty Chains to a black oak thence West thirty three Chains & fifty Links to a post Oak thence south sixty Chains to the Begining Containing by estimation 200 Acres

The reference to Morris/Moses Reed/Read/Road has not been resolved.

Table: Tax Listings for Jacob Frick

1803 Jacob Frick 200 A Capt. Lyarlie's Co. - Page 55

1807 Jacob Frek 200 A Capt. Creson's Co. - Page 124

1809 Jacob Frick 200 A Capt. Andrew Bower's Co. - Page 162

1810 Jacob Frick 200 A Capt. Bower's Co. - Page 179

1812 Jacob Frick 200 A Capt. Pool's Co. - Page 272

1813 Jacob Frick 200 A Capt. Pool's Co. - Page 330

1814 Jacob Frick 200 A Capt. Pool's Co. - Page 363

1815 Jacob Frick 200 A Capt. Ja. Pool's Co. - Page 23

1823 Jacob Frick Senior 200 300 - - Capt. Miller's Co.

Various records demonstrate that Jacob Frick joined Leonard Knup and moved to Union County IL in the 1820s. Again, no records exist of his disposition of the 200 acres, but Isaac Ribelin reports the 200 acres in the 1830 tax list for his militia company and continues to report the land in various tax listings through 1855.[4, 11, 12]

Table: Tax Listings for Isaac Ribelin

1830 - 1 WP 0 BP 200 - Capt. Isaac Riblen's Co.

1841 - 1 WP 0 BP 378 200 - Capt. Trexler's Co.

1842 - 1 WP 0 BP 378 200 - Capt. Trexler's Co.

1843 - 1 WP 0 BP 378 200 - Capt. Trexler's Co.

1844 - 1 WP 0 BP 378 200 - Capt. Trexler's Co.

1845 - 1 WP 0 BP 378 200 200(undivided) - Capt. Trexler's Co.

1846 - 0 WP 0 BP 578 200 - Capt. Trexler's Co.]

1847 - 0 WP 0 BP 378 200 200(undivided) - Capt. Trexler's Co.

1848 - 0 WP 0 BP 378 200 200(undivided) - Capt. Trexler's Co.

1849 - 1 WP 0 BP 379 332 200 - Capt. Levi Trexler's Co.

1855 - 378 on Panther Creek - Capt. Levi Trexler's Co.

In order to understand the tax records for Ribelin, we note that he only reports the 200-acre Frick Tract in 1830. By 1841, he has obtained the lands eventually sold to Reuben J. Holmes in deed DB45:84 dated 28 August 1869 after his death. That deed contains two tracts of land containing 150 acres and 28 acres. When combined with the Frick Tract, we calculate 378 acres as reported on the tax listings. We believe the additional 200-acre tract in 1841 is the northern portion of the Bame/Cauble tract from deed DB20:208. We discuss this tract below. We have not determined the origin of the additional 200 undivided acres reported in 1847 and 1848. By 1849 Ribelin reports an additional 132 acres. In any case by the 1840s, Isaac Ribelin is in possession of the plats labeled "48:84," "10:217," and "20:208" in Fig. 1 and shown outlined in green as Ribelin in Fig. 2. We note that the dower of his wife, Mary Eagle, is found in his estate folder dated 1863[5] and that the property described is the original Fennell/Frick Tract of land.

... beginning at a Pine thence East 33½ chains to a White Oak thence North 60 chains to a B.O. thence West 33½ chains to a P oak thence South 60 chains to the Beginning containing two hundred Acres with an exception of thirty five Acres previously conveyed to John E. Carter and David Trexlar leaving one hundred and sixty five Acres more or less.

The land excepted to David Trexler is part of a tract found in a deed dated 8 December 1852 of 200 acres from Isaac Ribelin to David Trexler. The metes and bounds are as follows:

On the waters of Panther creek, adjoining the lands of Horah, Wilson Morgan, Solomon Eagle, Isaac Riblin, and others, beginning at a stake in Horah's line, running North with his line 34 chains and 50 links to a small Red Oak bush in Wilson Morgan's line, thence West with his line 2 chains 25 links to a stake his corner, thence North with line 2 chains 50 lines to a old Black Oak in his line Eagle's corner, thence West with his line 46 chains 50 links to a small Pine on the bank of Panther Creek formerly a Maple his corner, thence South West on the said Creek as it meanders 28 chains 50 links to a small Hickory at the mouth of a small branch on the bank of said Creek, thence S 54o East 17 chains to a small Dogwood near a branch, thence East 46 chains and 25 links to the beginning, containing in all Two Hundred Acres of land.

A plat of the 200 acres is shown in Fig. 3 labeled "44:525" and outlined in red. The plat contains the upper section of the Bame/Cauble 200 acres described in deed DB20:208 and clearly indicates that Isaac Ribelin purchased the Bame/Cauble tract before selling the upper section to Trexler. We note again that the northern boundary is specified as the land of Solomon Eagle and serves as further proof that Eagle came into possession of the 207-acre tract.

Of considerable importance to our construction of the Panther Creek Plats is the statement that the upper right corner of the Trexler plat adjoins the property of Wilson Morgan. Fortunately, a deed exists dated 5 January 1847 in which Hugh Morgan, the father of Wilson Morgan, transfers 50 acres to him. The metes and bounds are described as follows:

Beginning at a stake in Cobles old Line running North 82 poles to a stake 1 small Post Oak near a Branch, thence East to a Hickory in Said old line near the Big Road 1 Post oak 1 Black Jack 98 Poles, thence South 82 poles to a stake in the said 2 Black Oaks Bush, thence West to the Beginning corner containing 50 acres.

The plat for the Morgan tract is shown in Fig. 3 labeled "35:55" and outlined in red. By the 1855 tax list of Capt. Levi Trexler,[4] David Trexler reports 250 acres on Panther Creek and we think he has obtained the 50 acres from Wilson Morgan along with his 200 acres from Ribelin. Further evidence that Trexler obtains the 50 acres is found in the division of the Boger Tract described below. We note that Wilson Morgan reports 118 acres on Reedy Branch in 1855, not Panther Creek!

The location of the Morgan tract implies that at least the lower section of the Edward Davis Tract has previously been sold. Indeed, a careful reading of deed DB23:875 dated 23 July 1816 in which Peter Lyerly sold 90 acres to Martin Miller shows that Enoch Phillips owns the lower section by the date on the deed.

… on the waters of Panter [sic] Creek beginning at a Post Oak Enoch Phillips old corner and running thence South eleven chains to a Red Oak, thence West fifteen chains to three Black Oaks, thence South ten chains to a Spanish Oak, thence West twenty five chains to a stooping White Oak, thence north twenty eight chains and fifty links along John Beams line to a Hickory Bush Enoch Phillips corner, thence with his line East forty chains to his corner a Post Oak in his line, thence with his line again south to the beginning containing in the whole ninety acres of land.

Prior to this deed, Peter Lyerly reported 150 acres in an 1803 tax record and 240 acres by 1809.[7] In his 1815 tax listing,[7] he specifically breaks his real estate into two pieces of 150 acres and 90 acres. We have not found a deed wherein Peter obtains the 90 acres. In a discussion below of the Boger Tract, we confirm that Enoch Phillips purchased the lower 100 acres of the Edward Davis Tract, although no records exist for the transaction. Furthermore, the tax records for Enoch Phillips are sparse and of little help as shown in the following table.[7]

Tax Listings of Enoch Phillips

1807 - 1 WP 0 BP 241 - Capt. Creson's Co. - Page 124

1809 - 1 WP 0 BP 241 - Capt. Andrew Bower's Co. -0 Page 162

1810 - 1 WP 0 BP - Capt. Bower's Co. - Page 179

As we indicated in our initial discussion of the real estate West of Panther Creek, there is a vacuum of information upon which one can proceed, but that progress can be made. It is useful to begin with the 1888 division of land of Jesse Ribelin, the son of Isaac Ribein.[5] Jesse died on 11 November 1874 according to his tombstone at the Saint Matthews Lutheran Church in Rowan County. In his estate folder labeled "Ribelin, Jesse 1874", a number of documents are found describing the division of his land. In the petition for the sale of his land, we find the following statement under item III:

That said land is situate in Rowan County adjoining the lands of George Bame, Nancy Huffman, Thos. Carter, Geo. Crotzer, Isaac Goodman, Moses Goodman, & other containing two hundred and two acres more or less.

For future reference in subsequent discussions below, we note that Moses Goodman is the son of Christopher Goodman and Amelia Knup.

The report of the Commissioners appointed to partition the land contains the metes and bounds for six lots that are divided among his children. Taking into account the fact that the surveyor reports the metes and bounds using lines that are slightly askew to the usual lines of the compass, we display the composite plat of the 202 acres in Fig. 2 outlined in red with the label "Jesse Ribelin." The metes and bounds for Lot No. 5 are of particular interest to us.

Lot No. 5 is assigned and appropriated to Jane Kluttz in severalty bounded as follows: viz: Beginning at a stake in the line of Lot No. 5 and running N 37½o E 15.28 chs to a stone in Bame's line, thence N 87o W 3.28 chs to a stone, Bame's corner, thence N 3½o E .85 chs to a pine knot, E. Lewis' corner, thence N 87 W 13.75 chs to a stone, Lewis' corner, thence N 3½o W 11.08 chs to a stake in a glade, thence N 87o W 8.32 chs to a stake, Goodman's corner, thence S 3½o W 26.52 chs to a stones corner to Lot No. 6, then S 87o E 24.13 chs to the beginning containing 47.70 Acres more or less valued at $171.00.

The first point to make is that the property of Jesse Ribelin adjoins the property of one "E. Lewis." This person is Eve Ann Lewis, the daughter of Jonathan Stoner and Esther Ludwick, whose third husband was John Lewis. She married John on 24 August 1868 in Lafayette County MS as reported in the ebook The Stoner Family of Rowan County.[6] In the 1879 division of the lands of Jonathan Stoner, Eve was alloted Lot No. 3, the southern leg of the plat labeled in Fig. 2 as "11:82"/13:719". This identification serves as one of the anchor points to connect the northern tier of plats in the Panther Creek Plats with the southern plats. We describe the Stoner plat in further detail below.

We note also from the description of Lot No. 5 that the northern border East of the Lewis property is the land of George Bame. Examination of the other lots in the division of Ribelin land shows that the full boundary East of the Stoner/Lewis plat adjoins to George Bame. We return to this point below when we determine the full scope of the Bame land.

Our next clue to creating plats for the property West of Panther Creek comes from tax records and is based on the information above that the land of Jesse Ribelin adjoins the property of George Crotzer from its southwestern corner East along a line to Panther Creek. To pursue that clue, we first examine the tax listings for Crotzer as shown in the following table.[4, 13]

Table: Tax Listings for George Crotzer

1841 - 1 WP 0 BP 90 - Capt. Trexler's Co.

1842 - 1 WP 0 BP 90.110 - Capt. Trexler's Co.

1843 - 2 WP 0 BP 90.110 - Capt. Trexler's Co.

1844 - 1 WP 0 BP 90.110 - Capt. Trexler's Co.

1845 - 1 WP 0 BP 90 - Capt. Trexler's Co.

1847 - 1 WP 0 BP 90 - Capt. Trexler's Co.

1848 - 1 WP 0 BP 90 - Capt. Trexler's Co.

1849 - 1 WP 0 BP 90 - Capt. Trexler's Co.

1855 - 242½ - Capt. Trexler's Co.

From 1841 through 1849, George pays the taxes for a 90-acre tract of land. Is this the 90-acre tract reported by Michael Stoner in 1815 and subsequently by his widow, Eve Stoner, until her death in 1836? We know that Henry Harkey was her administrator.

Administration on the estate of Eve Stoner decd granted to Henry Harkey — he gave bond with Jonathan Stoner in $100, and was qualified.

Rowan P&QS: May Term 1836, page 41

Rowan P&QS: May Term 1836, page 41

We know further that Jacob Harkey, the son of Henry Harkey, sold a 110-acre tract to Moses Earnhart on 6 September 1844 in deed DB38:65 with the following metes and bounds:

… lying on the west side of Panter [sic] Creek Beginning at a sassafras stake in Goodman's line thence South to a Post Oak stump in Ribelin's line thence East with Ribelin's line to Panther Creek Eagles corner thence down the meanders of the creek to Crotser corner a Whight Oak in Eagles line thence West along Crotser line to the beginning containing hundred and ten acres of land.

Although the exact dimensions of the plat are not given, a number of significant facts are present. First, we learn that the western boundary is the Goodman line. That fact matches with the history of the original Hess State Grants DB12:388 and DB13:722 which said property comes into the hands of the Goodman family. We will not review that history except to note that the property belongs to George Goodman from about 1830 into the 1850s.

We next learn from the Harkey to Earnhart deed that the southern border adjoins the land of Ribelin as we previously described above and that the border runs to Panther Creek and Eagle's corner and then down the meanders of Panther Creek along Eagle's line. This description locks into place our contention above that the 207-acre tract East of Panther Creek eventually becomes the property of Solomon Eagle.

It's important to note in the above description that the northeastern corner is "Crotser corner a Whight Oak in Eagles line." Both the Rendleman plat and the Kurtz plat for this corner display it as going all the way to the northwestern corner of the Eagle plat, but that is clearly not what the metes and bounds describe. Furthermore, the description portrays the northern border as "along the Crotser line to the beginning" in the Goodman line. Given the Jesse Ribelin plat and this Harkey/Earnhart plat, we must conclude that Crotzer owned property sandwiched in between these two plats. Is that possible?

In Fig. 2, we present our resolution of the above descriptions of metes and bounds with a rendering of the plats that satisfies all the known information. First, we insert a plat for George Crotzer that borders the Jesse Ribelin plat and whose northeastern corner connects with the northwestern corner of the Eagle property. Below that plat, we construct another plat by drawing a boundary line from the Goodman plat to Panther Creek along the Eagle line. A measurement of the area contained in the two plats indicates that the upper plat contains about 90 acres and the lower plat about 110 acres. We conclude that it is not only possible to insert a 90-acre plat for Crotzer, but that we must do so in order to cover the area West of Panther Creek.

Digging a bit deeper, we note from 1842 to 1844 that George Crotzer pays the taxes on two tracts, his 90-acre tract and a 110-acre tract. There can be little doubt that he is paying the taxes for the 110-acre Harkey/Earnhart tract before the tract is sold in 1844. Furthermore, Moses Earnhart pays the taxes for the 110 acres in 1848 but does not appear in the 1849 tax roll for Capt. Trexler's Company. By the 1855 tax list for Capt. Levy Trexler's Company, Moses Earnhart is no longer paying the taxes for the 110 acres. Instead, George Crotzer is paying for 242½ acres of land. Is he paying for the 110 acres and is the land now in his possession by 1855? No deeds exist confirming a transfer of the 110-acre tract to Crotzer, but it is easy to deconstruct the 242½ acres that he reports in 1855.

On 13 November 1853, George married a second time to Cynthia "Syntha/Scintha" H. Goodman Kirk, the daughter of George Goodman. George Goodman died in 1853 and his lands were divided on 22 February 1854. That division is reported in a document found in the Goodman estate folder.[14] Cynthia was alloted Lot No. 6 as follows:

Lot No. 6 allotted to Scintha H Crotser beginning at post oak the second corner of Lot No. 5 running E 15 Chs to a stone in Crotsers line, thence S with his line 29 Chs to a stone Kirks corner, thence West 15 Chs to a stake in his line to the corner of lot 5, thence N with the said line to the beginning containing in all 42½ acres be the same more or less valued at one hundred & forty dollars

The description of the metes and bounds of Lot No. 6 are important for two reasons. First, we learn that George Crotzer is responsible for 42½ acres over and above his 90 acres and that when the 110-acre tract is added in, we get 242½ acres as reported in 1855. Second, and equally important, we learn that the Crotzer line for the eastern border of Lot No. 6 runs all the way to the southeastern corner of the whole tract of the Goodman property. This corner must be on the line of the Harkey/Earnhart in order for the acreage of the 90-acre and 110-acre plats to be realized. This confirms that Crotzer is in possession of the Harkey/Earnhart Tract by 1854.

We conclude our discussion of the properties West of Panther Creek by examining the remaining tract of land directly West of the Jesse Ribelin Tract and shown in Fig. 3 labeled "Goodman?" and outlined in gold and described below as the "gold plat." The story begins with the 1854 division of the lands of George Goodman into lots.[14] The metes and bounds for Lots No. 7 and No. 9, the lots adjoining our "gold" tract of land, are as follows:

Lot No. 7 allotted to Caleb Goodman beginning at stone in Crotsers line, thence 2nd corner of lot No. 6 running N with Goodmans line 23.25 Chs to a stake in sd line the corner of lot No. 9, thence W the sd line of No. 9 19.25 chs to a stake of lot No. 8, thence S 23.25 Chs with the line of lot No. 8 to a stone in the line of lot No. 5, thence E 19.25 Chs passing the corner of lot No. 6 to the beginning containing in all 42½ acres of land be the same more or less valued at one hundred dollars.

Lot No. 9 allotted to John Goodmans Heirs beginning at stake in Goodmans line the corner of lot No. 7 running N with Goodmans line 8.75 Chs to a black jack oak his corner, thence W with C. Goodmans line 23.5 Chs to a post oak stump his corner, thence N 6.75 Chs to a stone his corner, thence W with his line 15.25 Chs to a stone in his line the corner of Lot No. 3, thence S with the line of lot No. 3 15 Chs passing the corner of lot No. 3 to a stake in the lot No. 2 near a Branch a corner of Lot No. 8, thence with the line of No. 8 and 7.38 chains to the beginning containing in all forty two & half acres be the same more or less.

Lot No. 9 allotted to John Goodmans Heirs beginning at stake in Goodmans line the corner of lot No. 7 running N with Goodmans line 8.75 Chs to a black jack oak his corner, thence W with C. Goodmans line 23.5 Chs to a post oak stump his corner, thence N 6.75 Chs to a stone his corner, thence W with his line 15.25 Chs to a stone in his line the corner of Lot No. 3, thence S with the line of lot No. 3 15 Chs passing the corner of lot No. 3 to a stake in the lot No. 2 near a Branch a corner of Lot No. 8, thence with the line of No. 8 and 7.38 chains to the beginning containing in all forty two & half acres be the same more or less.

We note that the eastern boundary of Lot No. 7 is described as "running N with Goodmans line 23.25 Chs to a stake in sd line the corner of No. 9." We interpret this phrase to mean that the property to the East belongs to a Goodman and hence "Goodmans line." The eastern boundary of Lot No. 9 which connects with Lot No. 7 to the North is described as "running N with Goodmans line 8.75 Chs to a black jack oak his corner" and once again implies that the property to the East belongs to a Goodman and that the corner is a Goodman corner. The description of the northern border West of the Goodman corner is particularly explicit: "thence W with C. Goodmans line 23.5 chs to a post oak stump his corner, thence N 6.75 Chs to a stone his corner, thence W … " We learn that our "gold plat" belongs to a "C. Goodman" which could be either Caleb or Christopher Goodman, sons of George Goodman. Caleb was born about 1840 and does not report any property in the 1855 tax list of Capt. Levi Trexler. On the other hand, Christopher Goodman reports two tracts of 42½ acres, Lot No. 5 from the division of his father's land, and 125 acres. Both tracts are on Reedy Branch but that is easily explained since Reedy Branch runs near the Western boundary of the George Goodman property thereby placing the Goodman property in the Reedy Branch watershed instead of Panther Creek. We believe that the 125-acre tract of Christopher Goodman contains our "gold plat."

Using the scale factors that underlie the drawing of our figures, we estimate the our "gold plat" contains approximately 92 acres of land leaving about 28 acres. That additional acreage is easily explained by noting from the description of Lot No. 9 in the division of George Goodman's land that the boundary for C. Goodman's property continues West from the "gold plat" and likely is made up out of a strip of real estate from the old Hess property. Unfortunately, no deeds or further evidence have been found to confirm our supposition, although it is interesting to note that in 1888 the land of Jesse Ribelin adjoins Moses Goodman, a son of Christopher Goodman. Other land transactions for the area following the Civil War often mention the property of a "Milly Goodman." Amelia "Milly" Knup was the wife of Christopher Goodman and he died in the Civil War.

It is also amusing to note that the combination of the "gold" 92 acres with the 202 acres of Jesse Ribelin add to 294, very close to the 300-acre tract reported by Michael Stoner and within our margin of error. Indeed, Christina "Teny" Stoner who married John Bame sold her one seventh interest in 336½ acres to her brother-in-law, John Knup in deed DB31:200 on 21 February 1831. The metes and bounds are as follows:

… on the waters of Panther Creek, bounded with George Waller line widow Caty Bame line with George Goodman Henry Harkey & Mihel Hofman being the seven part of three hundred and thirty acres and half

Elizabeth Trexler, the daughter of Peter Trexler, married George Waller and likely inherited part of the land on the northern border of the Michael Stoner property near Panther Creek following her father's death in late 1813 or early 1814. We discuss the Trexler property below. Goodman and Harkey border our "gold plat" with the Harkey property being along the northern boundary of the George Goodman property.

The reference to "Mihel Hofman" property bordering the 336½-acre tract is a story unto itself and begins with State Grant No. 960 of 200 acres to Robert Weakley in deed DB10:275 dated 4 May 1784 as shown in Fig. 1 and outlined in gold in Fig. 2. As described above, this plat of land is incorrectly rendered in both the Rendleman plat map and the Kurtz plat map. Furthermore, there are missing deeds as well as estate records in the sequence of the transition of the property from one owner to the next. We begin with the metes and bounds for the original grant and then tract the land through various deeds.

… on the waters of Reedy branch Beginning at a post Oak in Michael Pealors line runs along his line and past his corner south forty chs to a black Jack thence East fifty chs to a stake thence North forty chs to a stake thence west to John Pasingers corner and along his line to the Beginning

Weakley transfers the land to John Bullen on 18 August 1787 in deed DB11:207.

… on the waters of the Reedy branch Including the platation where sd, Bullin lived. Beginning at a white Post oak on Michael Pealor's line runs along his line & past his corner South forty chains to a black Jack East fifty chains to a stake thence north forty chains to a stake thence west to John Pasingers corner and along his line to the beginning containing two hundred acres

By 27 November 1793 in deed DB13:719, the land is mentioned in a State Grant to John Basinger as being the property of Thomas Basinger but no deeds exist showing the transition from John Bullen to Thomas.

… on the West Side of Panthers Creek beginning at a Spanish Oak corner to another tract belonging to said Basinger & Running thence with Thos Basingers line South forty Chs to a Stake thence with his line again West Six Chs to a Sasafras

We discuss the property of John Basinger below. For sure, we know that Thomas Basinger and his wife Margaret sell the 200-acre tract to Valentine Fogle in deed DB14:503 dated 17 October 1789.

… on the waters of Reedy Branch Beginning at a post oak on Michael Peelers line & runs along his line & past his corner South forty chs to a black jack thence East fifty chs to a stake thence North forty chs to a stake thence West to John Pasingers corner & along his line to the Begining being by estimation 200 acres

Although Thomas sells the property before the State Grant to John Basinger thereby causing some confusion as to why the State Grant describes the adjoining land as being Basinger rather than Fogle property, such inconsistencies often arise in deeds, especially given that the survey of the John Basinger grant could have been done several years before being filed and approved. In any case, we know that Thomas Basinger owned the 200-acre tract for a short period of time.

Valentine Fogle sold the same 200-acre tract to Frederick Fisher in deed 14:490 dated 28 December 1795.

… with waters of the Reedy Branch Beginning at a post Oak Michael Peelers line & runs along his line & past his corner South forty chs to a black Jack thence East fifty chs to a stake thence north forty chs to a stake thence west to John Basingers corner & along his line to the Beginning

Frederick Fisher died about 1798 according to his Rowan County estate records.[15] His son, Charles Fisher, sold the 200-acre tract to Michael Hoffman in deed DB20:419 dated 1 February 1814.

… on the waters of the Reedy Branch Beginning at a post oak Michael Pealors line & runs along his line & past his corner South forty chains to a Black Jack thence East fifty chains to a stake thence North forty chains to a stake, thence West to John Passingers corner & along his line to the Beginning Estimated two hundred acres

We note that the tax records for 1807 break out the land holdings of Charles Fisher into separate pieces of land and we find "Jacob Fisher Esq for Chas. Fisher 200" indicating that Charles did indeed obtain the land from his father.[7]

Based on an analysis of the land transactions of Michael Hoffman and his tax records through 1848, it appears that Michael possessed the 200-acre tract until his death on 18 February 1849. Unfortunately, the disposition of the real estate of Michael Hoffman is not known or found in his estate papers or in deeds. In any case, by examination of the 200-acre plat in Fig. 2, it is obvious that this Hoffman Tract adjoins the purported real estate of Michael Stoner and confirms the listing of "Mihel Hofman" in deed DB31:200 as presented above.

The reference to the widow Caty Bame in deed DB31:200 is confusing since there seems no way that her property, whose location is known, could have bordered that of Michael Stoner, although her son is George Bame and his property does border the Stoner — subsequently Ribelin — land. Furthermore, it is not clear why the property is reported as 336½ acres. Independent of these issues, we speculate that the "gold plat" plus the Jesse Ribelin Tract constitute the 300-acre tract of Michael Stoner.

Although convoluted and tedious from the careful analysis of the details and the language of the available information, it seems clear that our rendering of the plats West of Panther Creek is correct, consistent, and amazingly falls into place as a story. We turn next to the northern tier of plats in the Panther Creek Plats.

We begin with the two State Grants DB11:82 dated 25 October 1786 and DB13:719 dated 27 November 1793 to John Basinger. The metes and bounds of 11:82 are as follows:

… a tract of Land Containing 111 acres lying & being in the County of Rowan lying on the waters of second Creek Beginning at a Spanish Oak Michael Krights corner Francis Hofeman's line South 14 Chs Sapling said Hofemans corner thence Along his line West 10 Chs to a post Oak Sapling his corner along his line & past his corner South 25 Chs to a Black Oak thence East 32 Chs & 20 Links to a Spanish Oak thence North 39 [29?] Chs to a Stake on sd Krights line thence along his line West to the Beginning

Deed DB13:719 is described as follows:

… a tract of land Containing One Hundred and ten Acres lying & being in our County of Rowan on the West Side of Panthers Creek beginning at a Spanish Oak corner to another tract belonging to said Basinger & Running thence with Thos Basingers line South forty Chs to a Stake thence with his line again West Six Chs to a Sasafras then South ten Chs to a black Jack Oak then East twelve Chs to a Small pine in Peter Frixelers line thence with his line North Seventy two Chs & fifty links to a black Jack Oak in Michl Krits's line thence with his line four Chs & Seventy five links to his Corner post Oak then with Krites line again North fifteen Chains & fifty to his Corner Stake thence with Krites line Again fourteen Chains & twenty five links to a Stake the said Basingers Corner thence with his own line South to the Beginning

A combined plat for these two grants is shown in Figs. 1 and 2 with the label "11:82/13:719". John Basinger died in 1824 and Jonathan Stoner purchased the land at a public sale as described in deed DB28:653.

Whereas a decree was obtained in the Court of Equity for Rowan County at April Term 1824 directing the Clerk & Master of sd Court to expose to public sale the lands belonging to the heirs at law of John Basinger decd for the benefit of the Petitioners named in the petition filed in said Court. The Clerk and master in obedience to said decree exposed the said lands to public sale on the 16th day of August AD 1824 and Jonathan Stoner being the last and highest bidder became the purchaser

The metes and bounds are described as follows:

… two pieces or tracts of land lying and being in Rowan County on the waters of Dutch second Creek bounded as follows to wit, the first tract beginning at a Spanish Oak at a place in the original survey call Michael Krights corner and running agreeable to the original state grant along Frances Hoffmans line South fourteen chains to a post oak said Hoffmans corner thence along his line ten chains, thence along his line and past his corner South twenty five chains to a black oak thence East thirty two chains & twenty links to a Spanish Oak thence north thirty nine chains to a stake on said Krights line thence along his line West to the beginning containing one hundred and eleven acres more or less. The second tract bounded as follows to wit, Beginning at a Spanish Oak corner of the above mentioned tract and running thence with Thomas Basingers line to a stake Thomas Basingers corner thirteen chains East, thence with Thomas Basingers line South forty chains to a stake, thence with his line again West six chains to a sassafras, thence South ten chains to a black jack oak, thence East twelve chains to a small pine on Peter Trexlers line thence with his line North seventy two chains and fifty links to a black jack oak in the aforesaid Michael Krights line, thence with his line four chains and seventy five links to his corner a Post Oak thence with Krights line again North fifteen chains and fifty links to his corner a stake, thence with Krights line again fourteen chains and twenty five links to a stake the said Basingers corner, thence with his own line South to the beginning, containing one hundred and ten acres more or less, both tracts being adjoining and containing in all two hundred and twenty one acres together

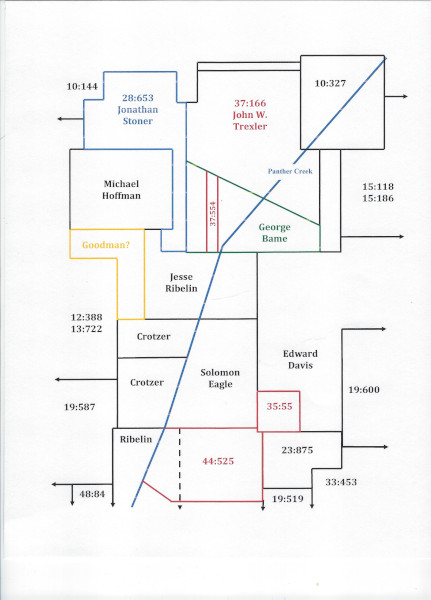

As pointed out above, the Rendleman plat map and the Kurtz plat map for this region of Morgan Township both incorrectly render this 221-acre tract of land. The correct rendering is shown in Fig. 3 labeled "28:653 Jonathan Stoner" and outlined in blue.

In the above description of the sell of the Basinger property to Jonathan Stoner, we note that the eastern boundary of the land runs "on Peter Trexlers line." Indeed, Peter Trexler obtained the 576-acre tract of land from Benedick Miller in deed DB16:160 dated 9 December 1797 with the following description of the metes and bounds.

… on Panther Creek Beginning at a post oak on the north side of said Creek Fredc Fishers corner, then along Fishers line East twenty Chains to a pine, thence south fifty chains to a Hickory, thence West seventy five Chains to a post oak thence north ninety five chains to a Black oak thence East fifty six Chains to a Stake on the said Fishers line thence along the same south to the Beginning Containing in the whole five hundred and seventy six acres

We display this tract of land in Fig. 1 with the label "16:160".

Before his death in late 1813 or early 1814, Peter sold the upper 346 acres of his property to his son, John Trexler, in deed DB23:744 dated 10 May 1813. The metes and bounds of that deed are as follows:

… on the waters of Panther Creek beginning at a stone and a small hickory in the West line of the old tract and running thence with the old line North twenty nine chains and twenty links to a Black Jack in Bullens line, thence with his line East five chains and fifty links to a Red Oak thence with his line again North fifteen chains and fifty links to a Persimmon Bush thence East fifty three chains and fifty links to a Black Jack sapling in Mathias Fricks line thence with his line south thirty nine chains and fifty links to a Post Oak, thence East nine chains and fifty links crossing Panther Creek to a White Oak Krites old corner on the Bank of Simonses Branch thence with the said Krites old line south thirty seven chains and eighty links to two White Oak sapling corner to the dividing line thence with the said line North sixty three degrees West crossing the Creek again to the place of beginning containing in the whole three hundred and forty six acres of land

We display the plat for DB23:744 in Fig.2 labeled "23:744" and outlined in blue. We note that a section on the upper left corner and along the top have been removed from the old tract as well as a section along the bottom eastern boundary. Although no deeds clearly account for the removal of this acreage, the property shows up in other deeds and can be accounted for in some measure.

The disposition of the lower portion of the original Peter Trexler Tract is not easily determined, but it is likely to have been divided following his death. We believe that he had a daughter named Elizabeth Trexler who married George Waller on 13 July 1802 in Rowan County. As mentioned herein, George Waller is presented as owning property that matches with his real estate being in this lower section. We know from estate records that a George Waller died about 1824 with a widow named Elizabeth. Estate records[16] indicate that a petition was filed to sell his property on the South Fork of Crane Creek, but no mention is made of land on Panther Creek. On the other hand, we know that an Elizabeth "Betsy" Waller married Andrew Casper on 26 March 1831, that they were listed on the petition to sell the land of George Waller, and that they sold a 22-acre tract to George Bame in deed DB37:554 dated 4 May 1846 with the following metes and bounds.

… beginning at a stake on Stoners line corner to lot No. 2 running thence with Stoner's line East five chains and sixty links to a persimmon corner to No. 4 thence with the line of No. 4 North thirty-eight chains and ten links to a red oak on John Trexlers line thence along the line of No. 2 South forty one chains to the beginning containing Twenty Two acres of land

We display this plat of land in Fig. 3 labeled "37:554" vertically and outlined in red for the western and eastern borders. We note that the southern border is "Stoner's line" in conformity with our discussion above of the Jesse Ribelin plat being originally the Stoner property and the eastern portion of the northern border of the Ribelin plat adjoining the land of George Bame. It is of interest also to note the lot numbering which implies that the lower portion of the original Peter Trexler land was subdivided into lots, likely following either his death or the death of George Waller.

John Trexler, the son of Peter Trexler and grantee of the 346-acre tract, married Elizabeth Morgan, the daughter of Nathan Morgan and Naomi Pool, on 9 February 1813 in Rowan County. John died in 1829 according to his estate papers and court records.[17] His widow died in 1849.[18] Several of his heirs, namely "George Bame and Levina his wife, Levi Casper and Nayomy his wife and Elizabeth Trexler and Solomon Casper and Rachel his wife" sell their "interests in our father John Trexler's dec'd" 346-acre tract to John W. Trexler, a son of John Trexler and Elizabeth Morgan, in deed DB37:166 dated 4 May 1844 with the following metes and bounds.

… on the waters of Penter creek, beginning at a stone and a small hickory in the West line of the do tract, and running thence with the old line North twenty-nine chains and twenty links to a Black Jack in Bullen's line, thence with his line five chains & fifty links to a Post oak, thence with his line again North fifteen chains & fifty links to a persimmon bush thence East fifty three chains & fifty links to a Black Jack saplin in Matthias Frick's line, thence with his line South thirty-nine chains and fifty links to a Post-oak, thence East nine chains and fifty links crossing Panter [sic] creek to a white oak Leonard Hofner corner on the bank of Simon's branch, thence with said Hofner's old line South thirty- seven chains and eighty links to two white oak saplings corner to the dividing line now called George Bame's line, thence with his line North sixty-three degrees West crossing the creek again to the place of beginning, containing in the whole three hundred & forty six acres of land

It is important to note that the "dividing line" or southern boundary is "now called George Bame's line." We recall that the eastern portion of the northern boundary of the Jesse Ribelin plat is also George Bame's line and that Andrew Casper sold 22 acres to George in 1846. We ask whether or not George owned all of the lower portion of the Trexler land?

Tax Listings of George Bame

1841 - 1 WP 0 BP 168 - Capt. Trexler's Co.

1842 - 1 WP 0 BP 168 - Capt. Trexler's Co.

1843 - 1 WP 0 BP 168 - Capt. Trexler's Co.

1844 - 1 WP 0 BP 168 - Capt. Trexler's Co.

1845 - 1 WP 0 BP 168 - Capt. Trexler's Co.

1846 - 1 WP 0 BP 200 - Capt. Trexler's Co.

1847 - 1 WP 0 BP 200 - Capt. Trexler's Co.

1848 - 1 WP 0 BP 200 - Capt. Trexler's Co.

1849 - 1 WP 0 BP 200 - Capt. Trexler's Co.

1855 - 275 A and 88 A on Panther Creek - Capt. Levy Trexler's Co.

We note that his real estate increases by 32 acres in 1846 to 200 acres. This would appear to agree with his purchase of the Andrew Casper Tract although the deed reports 22 acres sold. We have no explanation for the discrepancy.

On the other hand, the total of 200 acres would appear to constitute the entire lower portion of the Peter Trexler property. To substantiate the validity of such a claim, we note that John Trexler reported 346 acres in the 1813 tax lisings of Capt. Pool's Company.[7] In 1814 in the tax listings of Capt. Pool's Company, following the death of his father Peter, he reports his 346 acres plus 200 acres "for P. Trexler dec'd."[7] A similar record is found in the 1815 tax listings for Capt. Pool's Company with the phrase modified to "for his father."[7] These tax listings clearly indicate that the lower portion of the Peter Trexler property was 200 acres in agreement with the 200 acres reported by George Bame in the late 1840s. We conclude that George Bame possessed the lower portion of the Peter Trexler Tract. That tract is displayed in Fig. 3 labeled "George Bame" and outlined in green.

We turn next to the eastern border of the Peter Trexler plat. In deed DB15:118 dated 7 March 1795, David Woodson sells 318 acres to Michael Krite with the metes and bounds described as follows:

Beginning at a post Oak David Woodsons corner Running thence South Twenty chains to a black oak thence west 20 chains to a sweet Gum Thence south twenty three Chains & Twenty five links to a sassafras thence West 40 chains to a stake in Trexellers line thence north forty three chains & fifty links to a stake in Frederick Fishers line thence with his line East twenty eight Chains to a post Oak said Fishers corner thence with Fishers line again north 26 chains & 75 links to a pine on the south bank of Panther Creek thence east thirty seven Chs to a small red oak thence to the Beginning Containing in the whole 318 Acres of land

In deed DB15:186 dated 11 July 1797, Michael Krite transfers the land to Martin Hofner with the following description of the metes and bounds.

Begining at a post Oak David Woodsons corner, & runing thence South twenty chains to a black oak thence west 20 chains to a sweet Gum Thence south twenty three Chains & Twenty five links to a sassafras thence West forty chains to as stake in Trexlers line thence north forty three chains & fifty links to a stake Fredc Fishers old line thence with his line East twenty eight Chains to a post Oak his corner thence with his line again north twenty six chains & seventy five links to a pine on the south bank of Panther Creek thence east thirty seven Chains to a small red oak thence to the Begining Containing in the whole 318 Acres of land

In subsequent deeds, the property increases in acreage and is sold in several parts. In deed DB20:528 dated 1 March 1812, Martin Hofner sells the upper right part to his son John Hofner with the metes and bounds described as follows:

… on Panther Creek beginning at a Pine one of the old corners in Mathias Fricks line on the South side of the Creek and running thence East crossing of the Creek two times thirty eight chains and twenty five links to a small Spanish Oak the old corner thence South twenty eight chains and fifty links to a Post Oak the Beginning corner of the whole old tract thence West fifteen chains and fifty links to two small Post Oaks thence South thirty six degrees West seven chains and twenty links to Post Oak near the Jas [?] Marks Branch, thence North fifty five degrees West twenty two chains and seventy five links to a small Post Oak in the aforesaid Mathias Fricks line thence with his line North to the Beginning containing in the whole one hundred and eight acres of land

In deed DB33:326 dated 14 October 1834, Henry Hofner sells the middle part to Leonard Hofner with the metes and bounds described as follows:

… on the waters of Panther Creek Beginning at a Post Oak and running thence West fifteen chains and 50 links to two small post oaks thence South thirty six degrees West seven chains and twenty links to a Post Oak thence North fifty five degrees West twenty two chains and seventy five links to a small Post Oak in Mathias Fricks line thence with his line South thirty chains and fifty links to a Red Oak his corner in George Hofners line thence with his line East six chains and twenty links to a light wood stake his corner thence with his line again South twenty seven chains and 75 links to a small Black Jack his corner in Hofners line thence East 12 chains and 75 links to a Siller Oak and a sweet gum thence East 20 chains to a Red oak the old corner thence North 20 chains to the Beginning containing 109 acres of land

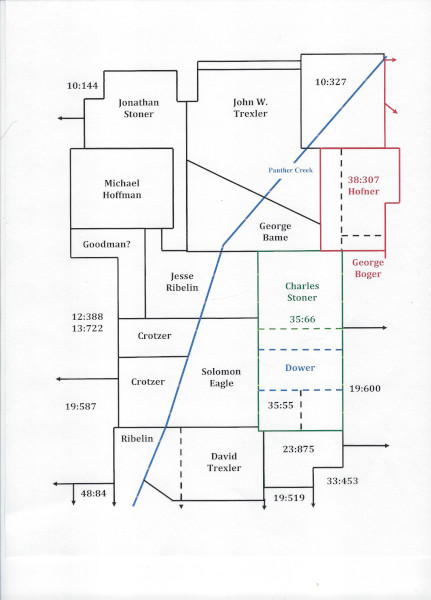

The most important deed and the one most relevant to our discussion is deed DB38:307 dated 17 March 1841 between Henry Messimore and Leonard Hofner in which 225 acres are transferred with the following metes and bounds.

Beginning at a light wood stake Leonard Hofner corner thence West to the bank of Simon's branch corner of Trexler's heirs in fricks line thence South fifty chains & 96 links, to a stake George Bogers corner in Bogers line then East to a state Bogers corner thence with Bogers line South 14 chs 60 linkes to a white oak in Bogers line thence East 6 L to a Black Oak corner of Michael Hofmans thence with 28 chs 25 links to a heap of stoners in Michael Hofmans Corner thence East about five chains to Leonard Hofners corner thence North With Leonard Hofners line 27 chains & 75 links to the Beginning containing in all two hundred and twenty five

In Fig. 4 we display our rendering of this plat with the label "38:307 Hofner" outlined in red. We note that the name "George Boger" is associated with the southern boundary, but no other records have been found placing Boger in possession of that property. We point out also that the eastern boundary of the original Peter Trexler Tract is shown as a vertical dashed line East of the red vertical dividing line between the later boundary of the Trexler property and the Hofner property line in deed DB38:307. The transfer of land and movement of plat boundaries in this region over time are complicated by the lack of deeds or other records, but it is clear that Hofner is in possession of the land outlined in red by 1848.

South of the properties of George Bame and Leonard Hofner is the land labeled "Edward Davis" in Figs. 1, 2, and 3. No deeds or other records exist to determine the upper border of the Davis Tract or the land immediately East of the Stoner/Ribelin Tract. We have previously pointed out that the southern part of the Davis Tract came into the hands of Enoch Phillips with the southwestern section of the same being deeded to Wilson Morgan in 1847 and almost certainly in the possessions of David Trexler by 1855. On the other hand, we do have the tax records for Edward Davis as reported in the following table.[7]

Tax Listings of Edward Davis

1803 - 1 WP 0 BP 270 - Capt. Lyarlie's Co. - Page 55

1807 - 1 WP 0 BP 210 - Capt. Creson's Co. - Page 124

1809 - 1 WP 0 BP 265 - Capt. Andrew Bower's Co. - Page 162

1810 - 1 WP 0 BP 270 - Capt. Bower's Co. - Page 178

1812 - 1 WP 0 BP 275 - Capt. Pool's Co. - Page 272

1813 - 1 WP 0 BP 275 - Capt. Pool's Co. - Page 330

1814 - 1 WP 0 BP 265 - Capt. Pool's Co. - Page 363

1815 - 1 WP 0 BP 275 (165.110) - Capt. Ja. Pool's Co. - page 23

In the 1815 tax listing, Davis reports his real estate as two tracts of 165 acres and 110 acres, but we don't know the location or the metes and bounds.

The first deed or land activity for the Davis Tract occurred on 8 December 1841 with the allotment of a Dower to Margaret or "Crate" Boger, the wife of Daniel Boger who died in 1826. The Dower transaction was followed on 1 February 1842 by deed DB35:66 wherein Reubin Harkey and his wife Margaret, formerly Boger, sold their share in two tracts of land to Charles Stoner. We begin with deed DB35:66 and the following metes and bounds for the first tract.

… the eight part of that tract of parcel of land … lying on the waters of Panter [sic] Creek beginning at a Black Oak George Bullons old corner & running thence two chains & fifty links to a small hickory then South two chs & seventy five links to a hickory grub, thence east forty chains to a post oak then North fifty chains & twenty five links to a spanish oak sapling in the aforesaid Bullons line thence with the same south to the beginning containing two hundred and ten acres of which one hundred acres is excepted lying on the South line which was taken off and deeded to Enoch Phillips

The description of this tract of land is reasonably straightforward but contains the condition that 100 acres have been excepted on the southern border to Enoch Phillips. This conforms with the language of deed DB23:875 along the southern border and the land transactions for the 50-acre tract involving Wilson Morgan and David Trexler. What makes this interesting in some measure is that the "exception" had already occurred by 1816, long before the 1842 deed, but consistent with the death of Daniel Boger in 1826. Furthermore, the deed describes Margaret Boger's share as an eighth share, even though there are ten heirs as will become clear below. We do not have an explanation for this discrepancy.

Of equal interest is the second tract of land in deed DB35:66 which serves to locate the land relative to the plats in our Panther Creek Plats. The metes and bounds are as follows:

… also one other tract of land adjoining the above tract … on the waters of Panter [sic] Creek beginning at a small Post Oak stump Edward Davises old corner in Mulls field and running with the said line North five chains and forty four links to a pine Mulls corner joined to Stoners land in all thirty eight chains & sixty nine links to a stake in a road in Trexlers line thence east forty two chains to a hickory his corner thence with his old line west to the beginning containing containing [sic] one hundred & sixty four acres of land

We display the second 164-acre tract in Fig. 4 as the upper portion of the plats outlined in green and running to the dashed horizontal line just below the label "35:66". The plat for the first 210-acre tract of land in deed DB35:66 runs from the same dashed line South past the section labeled "Dower" and contains the 100-acre southern portion excepted to Enoch Phillips. Thus the total acreage of the two tracts outlined in green is 374 acres.

The 164-acre tract is of some interest since it clearly describes the original Mull/Stoner corner which in Fig. 4 has become the Eagle/Ribelin eastern corner. The northern border is on the Trexler line running East "to a hickory his corner." When properly drawn, this corner proves to be the southeastern corner of the original Trexler Tract obtained from Benedict Miller in deed DB16:160 and shown by the vertical dashed line in Fig. 4. Both the Rendleman plat map and the Kurtz plat map for Morgan Township display the 164-acre tract as being moved East and above the plat labeled "19:600". Their rendering clearly does not fit known facts.

A description of the Dower for "Crate" Boger can be found in the estate records for her husband, Daniel Boger.[20] The Dower contains two tracts of land with the second tract being part of our discussion and with the following metes and bounds.

Also one other tract on the waters of Panther Creek Beginning at a (Black Oak Sol Eagles corner and runs East 40 poles to a Stake thence South 10 poles to a stake) Stake thence East 166 poles to a stakePost Oak Thence N 80 poles to a Post Oak thence West 176 poles to a stake thence south to the Beginning containing ninety acres

What makes this description interesting is that the surveyor initially started out describing the southwestern corner of the Enoch Phillips exception but crossed that out and began at the southwestern corner with the 100-acre tract excepted. We display the Dower plat in Fig. 4 between two dashed horizontal lines and labeled "Dower".

On 30 August 1845 in deed DB37:334, Charles Stoner obtains another share in the Boger Tract from Miles Mowry and his wife Christena, formerly Boger, which is described as follows:

… on the waters of Panther Creek Beginning at a Black oak George Bullens old corner then East 2 chs 50 links to a small Hickory then S 2 chs 75 links to a hickory bush then E 40 chs to a Post oak then N 50 chs 20 links to a spanish oak saplin in the aforesaid Bullens line then with the same South to the Beginning containing in all two hundred and seventy four acres be the same more or less and the one tenth part of which the said Miles Mowry and his wife Christena Mowry as one of the Heirs at Law of Daniel Boger Decd conveys to said Charles Stoner his Heirs and assigns containing twenty nine and a half acres of land be the same more or less and it is expressly instructed that this is the one tenth part of this said tract of land

This plat description has a number of issues. First, it is clearly the first tract from deed DB35:66 which contains 210 acres with 100 acres excepted to Phillips. On the other hand, the reported 274 acres represents the total tract of 374 minus the 100 acres to Phillips and doesn't match with the plat dimensions. Second, the share is now one tenth instead of one eighth. One tenth is the correct number as we will see below upon division of the land. Finally, we note that a one tenth share that equals to 29½ acres implies that the whole tract is 295 acres, not 274 acres.

On 1 August 1853 in deed DB40:57, Peter Peeler and his wife Eve, formerly Boger, sell their share of the Boger Tract to Charles Stoner as follows:

… all their undivided interest in a tract of land belonging to the heirs at law of Daniel Boger decd lying on the waters of Panther Creek containing two hundred and seventy four acres more or less one interest in said tract of land being one tenth or 27½ acres

Once again there are ten heirs but the share is described as 27½, not 29½. Furthermore, the metes and bounds are not specified.

At this point in our presentation, it is useful to review the tax records for Charles Stoner.[4, 21]

Tax Listings for Charles Stoner

1841 - 1 WP 0 BP - Capt. Trexler's Co.

1842 - 1 WP 0 BP - Capt. Trexler's Co.

1843 - 1 WP 0 BP - Capt. Trexler's Co.

1844 - 1 WP 0 BP 274 - Capt. Trexler's Co.

1845 - 1 WP 0 BP 274 - Capt. Trexler's Co.

1846 - 1 WP 0 BP 274 - Capt. Trexler's Co.

1847 - 1 WP 0 BP 274 - Capt. Trexler's Co

1848 - 1 WP 0 BP 274 - Capt. Trexler's Co.

1849 - 1 WP 0 BP 274 - Capt. Trexler's Co.

1855 - 137 A [Sic: should be 147] on Panther Creek - Capt. Trexler's Co.

Beginning with the year 1844, Stoner clearly pays the taxes for the Boger Tract minus the 100-acre exception to Phillips. As we point out below, the 274 acres should have been 295 acres. By 1855 following the division of the Boger Tract described below, Charles pays for his five shares which compute to 147½ acres. We assume the 137 acres reported in 1855 is an error.

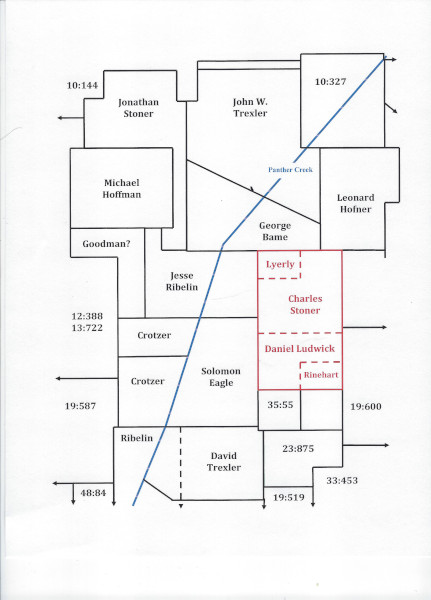

Margaret "Crate" Boger died on 28 September 1853 leaving behind ten heirs. One of her daughters, Sarah "Sally" Boger married John Rinehart on 30 September 1828 and her family unit owned one share of the land in the Boger Tract. Another daughter, Rachel Boger, married Zachariah Lyerly on 12 October 1833 and her family owned one share of the Boger Tract. The remaining eight heirs sell five shares to Charles Stoner with three of the shares documented in the deeds previously discussed and three shares to Daniel Ludwick. Other than the three reported Stoner deeds, no other deeds have been found to document the transfer of shares.

Following the death of Margaret, the land of Daniel Boger deceased was divided into ten shares and a number of court documents report the division.[22]

This plot of land represents a piece or part of the land called the Old Boger Tract divided among the several shares or claimants by a order of court, bounded as follows, to wit: lying on the waters of Panter [sic] Creek, adjoining the lands of Jesse Riblin and George Bame, beginning at a small spanish oak, J. Riblin's corner in George Bame's line, running South with Riblin's line 14 chains to a stake in said line; thence East 21 hains and fifty links to a pine, thence North 14 chains to a small hickory in Bame's line, thence West 21 chains and 50 links with Bame's line to the beginning, in all twenty nine and half acres of land, be the same more or less, valued at forty four dollars and twenty-five cents, the above lot allotted to Lyerls children.

This plot of land represents a piece or part of the lands called the Old Boger Tract, divided among the several shares, or claimants by a order of court bounded as follows, to wit, lying on the waters of Panther Creek, adjoining the lands of Jesse Ribelin, L. Hofner and others, beginning at a stake a corner of lot No. 1 in Jesse Riblins line, running South with his line 28 chains to a stone pile in Solomon Eagle's line near a branch; thence East 42 chains 75 links to a stake in Morgan's line near ahead of a branch; thence West with his line 21 chains and 50 links to a hickery in George Bame's line, a corner of lot No. 1: thence South with the line of No. 1 14 chains to a pine, a corner of said lot; thence West with said line 21 chains 50 links to the beginning, in all one hundred and forty-seven and a half acres of land, be the same more or less. The above plot represents five shares of twenty nine and a half acres of land each.

The above lots, allotted to Charles Stoner, valued at the whole at two hundred and twenty-seven dollars

This plot of land represents a piece or parcel of lands called the Old Boger Tract, divided among the several shares or claimants by a order of court, bounded as follows, to wit, lying on the waters of Panther Creek, adjoining the lands of Solomon Eagle, David Trexler, and others, beginning at a stone pile, a corner of No. 6[?] in Solomon Eagle's line near a branch running South with his line 58 chains to a stake, David Trexler's corner; thence East with his line 21 chains 50 links to a small sweet gum in said line; thence North 14 chains to a stake; thence East 21 chains 50 links to a stake in Morgan's line; thence North with Morgan's line 14 chains to a stake, a corner of lot No. 6, in said line; thence West with the remaining in all eight-eight and a half acres of land, be the same more or less. The above plot represents three shares of twenty- nine and a half acres of land each.

The above lots allotted to Daniel Ludwick, valued at one hundred and twenty-six dollars and seventy five cents.

This plot of land represents a piece or parcel of the lands called the Old Boger Tract, divided among the several shares or claimants by a order of court, bounded as follows, to wit: lying on the waters of Panther Creek, adjoining the lands of David Trexler, Hugh Morgan and others, beginning at a small gum, a corner of lot No. 9 in David Trexler's line running East with his line 21 chains 50 links to a post oak Hugh Morgan's corner, thence North with Morgan's line 14 chains to a stake, a corner of lot No. 8, in said line, thence West with the line of No. 8 21 chains and 50 links to a stake, a corner of said lot, thence South with the line of No. 9 14 chains to the beginning, containing in all twenty nine and a half acres of land, be the same more or less. The above lot alloted to Rinehardt children, valued at forty four dollars and twenty five cents.

This plot of land represents a piece or part of the lands called the Old Boger Tract, divided among the several shares, or claimants by a order of court bounded as follows, to wit, lying on the waters of Panther Creek, adjoining the lands of Jesse Ribelin, L. Hofner and others, beginning at a stake a corner of lot No. 1 in Jesse Riblins line, running South with his line 28 chains to a stone pile in Solomon Eagle's line near a branch; thence East 42 chains 75 links to a stake in Morgan's line near ahead of a branch; thence West with his line 21 chains and 50 links to a hickery in George Bame's line, a corner of lot No. 1: thence South with the line of No. 1 14 chains to a pine, a corner of said lot; thence West with said line 21 chains 50 links to the beginning, in all one hundred and forty-seven and a half acres of land, be the same more or less. The above plot represents five shares of twenty nine and a half acres of land each.

The above lots, allotted to Charles Stoner, valued at the whole at two hundred and twenty-seven dollars

This plot of land represents a piece or parcel of lands called the Old Boger Tract, divided among the several shares or claimants by a order of court, bounded as follows, to wit, lying on the waters of Panther Creek, adjoining the lands of Solomon Eagle, David Trexler, and others, beginning at a stone pile, a corner of No. 6[?] in Solomon Eagle's line near a branch running South with his line 58 chains to a stake, David Trexler's corner; thence East with his line 21 chains 50 links to a small sweet gum in said line; thence North 14 chains to a stake; thence East 21 chains 50 links to a stake in Morgan's line; thence North with Morgan's line 14 chains to a stake, a corner of lot No. 6, in said line; thence West with the remaining in all eight-eight and a half acres of land, be the same more or less. The above plot represents three shares of twenty- nine and a half acres of land each.

The above lots allotted to Daniel Ludwick, valued at one hundred and twenty-six dollars and seventy five cents.

This plot of land represents a piece or parcel of the lands called the Old Boger Tract, divided among the several shares or claimants by a order of court, bounded as follows, to wit: lying on the waters of Panther Creek, adjoining the lands of David Trexler, Hugh Morgan and others, beginning at a small gum, a corner of lot No. 9 in David Trexler's line running East with his line 21 chains 50 links to a post oak Hugh Morgan's corner, thence North with Morgan's line 14 chains to a stake, a corner of lot No. 8, in said line, thence West with the line of No. 8 21 chains and 50 links to a stake, a corner of said lot, thence South with the line of No. 9 14 chains to the beginning, containing in all twenty nine and a half acres of land, be the same more or less. The above lot alloted to Rinehardt children, valued at forty four dollars and twenty five cents.

The division of the land is shown in Fig. 5 outlined in red and the division into the four allotments displayed with the names of the dividends.

In this division of the Boger Tract, each share contains 29½ acres for a total of 295 acres. When properly drawn, we find that this acreage along with the 100 acres excepted to Enoch Phillips approximately matches the open space which we labeled as Edward Davis in previous plat images. We presume that some of confusion in earlier deeds from the 1840s resulted from the early death of Daniel Boger in 1826 and the fact that several decades passed before the "Old Boger Tract" was finally divided. Furthermore, it is clear that Charles Stoner did not get full ownership of the 164 acres in deed DB35:66 as Rendleman and Kurtz supposed, but merely a share in the undivided land. Whatever the case may be for the Boger Tract in the 1840s, the final resolution from the division of the land in 1855 is quite clear.

We have reported above the tax records for Charles Stoner and indicated that they are consistent with the deeds and the division of the Boger Tract. For Daniel Ludwick, we find that he reports 83 acres in the 1855 tax listing for Capt. Levi Trexler's Company,[4] although his three shares in the Boger Tract add to 88½ acres. The final two lots are reported together in the same 1855 tax listing as "Rinehart John & Zacariah Lyerly's Children on Panther Creek 54" acres instead of the 59 acres allotted from the division. Although minor errors exist in the actual acreage reported, the 1855 tax listing is consistent with the division of the Boger Tract.

Subsequent to the division of the Boger Tract, Charles Stoner and his wife Leah leave Rowan County and move to Vienna, Johnson County IL before 1860 apparently transferring ownership of the 147½ acres to Milas P. Morgan. We have described the property of Milas P. Morgan in The Stoner Family of Rowan County.[6]

Although glitches exist in the various records for the individual plats found in our Panther Creek Plats, they are mostly minor ones and don't substantially affect our rendering of the history of the land involved. We believe that our rendering in Fig. 5 is an accurate representation of the Panther Creek Plats in the late 1840s and mid 1850s.

We conclude by saying that we believe that the above analysis correctly presents the location of the property of Michael Stoner and the Boger Tract.

ENDNOTES

1. The Heritage of Rowan County, published by The Genealogical Society of Rowan County, North Carolina. This volume contains numerous examples of the Rendleman maps showing various sections of Rowan County. Original copies of the maps are available in the McCubbins Collection available at the Rowan Public Library, Salisbury, NC.

2. Rowan County Maps at NCSA: Early Landowners of Rowan County, by James W. Kluttz, Call Numbers MC.085.1995k.01 through MC.085.1995k.06. These six plat maps are available digitally from the North Carolina State Archives for a small price.

3. Rowan County, North Carolina, Tax Lists 1757-1800, Annotated Transcriptions, by Jo White Linn, Library of Congress Catalogue Card Number 95-81908, ISBN 0-918470-24-2, available at the History and Genealogy Department, Rowan Public Library, Salisbury NC.

4. Rowan County Tax Records CR085.701.7 NCSA, Folder: Tax Records 1855, Assessment — Capt. Levi Trexler Company, May Term 1855.

5. See the Commissioner's Report on division of the land of Jesse Ribelin dated 8 March 1888 and found misfiled in the Estate file for his father: Rowan County Estate Records CR.085.508.135 NCSA, Rendleman — Rice, File Folder: Ribelin, Isaac 1863. For additional documentation, see also Rowan County Estate Records CR.085.508.135 NCSA, Rendleman — Rice, File Folder: Ribelin, Jesse 1874.

6. See The Stoner Family of Rowan County by Keith McDowell at Amazon.

7. Rowan County, North Carolina, Tax Lists 1802-1814, Volumes One and Two, from the collection of Jo White Linn, available at Rowan Public Library, Salisbury NC; 1815 Rowan County, North Carolina, Tax List by Jo White Linn, C.G. 1987, available at Rowan Public Library, Salisbury NC

8. Rowan County Estate Records CR085.508.23 NCSA, Folder: Knup, John 1862

9. Rowan County Tax Records, 1758-1879, 1910 and undated, 1820-1839, CR.085.701.6 NCSA, File Folder: Tax Records 1838

10. Rowan County Tax Records, 1758-1829 CR085.701.5 NCSA, Folder: Tax Records 1820-1823, Capt. M. Miller's Co. for 1823.

11. Rowan County Tax Records, 1758-1829 CR085.701.6 NCSA, File Folder: Tax Records 1830, Capt. Isaac Riblens Company;

12. Rowan County Tax Lists 1841-1849 CR.085.701.4 NCSA. See pages 40, 63, 103, 178, 255, 298, 318, 377, and 420.

13. See Endnote [12], pages 39, 61, 101, 176, 253, 315, 373, and 414.

14. Rowan County Estate Records (downloaded from Family Search), File Folder: Goodman, George 1853.

15. Rowan County Estate Records (downloaded from Family Search), File Folder: Fisher, Frederick 1798.

16. Rowan County Estate Records (downloaded from Family Search), File Folder: Waller, Georgy 1824.